- Morning VC Brief

- Posts

- Deep Dive in 2025 AI VC Investment Landscape

Deep Dive in 2025 AI VC Investment Landscape

eric gu

January 06, 2026

Morning VC Brief is an expert daily curation of tech and venture news. Feel free to forward; the sign-up is here

Table of Contents

Overview: 2025 EOY Top VC AI Investment Review

Methodology and Market Context

This retrospective follows the logic established in our previous years' analyses. We selected over 20 top-tier institutional investors and aggregated their disclosed AI deals from 2025. To ensure a focus on high-potential startups, we filtered for companies completing Seed rounds within 3 years of founding, Series A/B within 5 years, and Series C+ within 7 years. This rigorous screening resulted in a sample size of 392 companies.

The Broader Market vs. Top-Tier Velocity

To contextualize our findings, we refer to recent market data from SVB (bottom left chart), which tracks US VC-backed startups. The "Graduation Rate" is currently at a 10-year low. For instance, while 22% of companies that raised a Seed round in 2020 reached Series A within three years, that figure dropped to less than 9% for the 2022 cohort. At current median rates, a company now takes approximately 10 years to scale from Seed to Series D—a 50% increase compared to 2022.

However, our dataset—representing the top 10% of the market backed by elite firms—tells a different story of hyper-growth. While calculating the gap between average ages (e.g., Average Series B Age minus Average Series A Age) is an approximation, the trend is undeniable. Notably, the progression from Series A to Series B took an average of only 8.28 months. This aligns with our on-the-ground observations and tracking of top-tier projects (such as those from YC), where it is becoming common to see "star" companies close two or even three rounds of financing within a single year.

The bar chart (right) compares deal sizes against a baseline of PitchBook’s 2025 North American median data. The dark blue bars represent the median premium for general AI deals (SVB data), while the light blue bars represent the premium for our "Selected" top-tier AI companies. The data reveals a significant "AI Premium" in both deal size and implied valuation. While there is little differentiation at the Seed stage, a massive divergence appears at the scaling stages (Series A onwards). The fundraising capability of top-tier AI startups significantly outperforms both the general market and the broader AI sector.

Seed - Established For Less Than 3yrs

Market Overview In the Seed stage cohort (startups established for less than 3 years), the Application layer dominates by volume.

Vertical AI specifically accounts for nearly 50% of the total sample. Consistent with trends seen in Series A/B, Finance and Healthcare remain the most populated sectors.

Finance AI: The primary focus is process automation for corporate finance, covering Tax, Bookkeeping, Accounts Receivable, and Compliance. We also see platforms dedicated to improving investment research efficiency/insights and productivity tools for CPAs.

Healthcare AI: The majority of startups are tackling administrative and operational inefficiencies rather than diagnostics. Key use cases include automating insurance verification, patient admission flows, and eligibility checks.

Legal AI: With generalist leaders like Harvey and Legora already at later stages, early-stage opportunities have shifted to niche scenarios. We are seeing a cluster of startups focused on Patent/IP protection and specific workflows for M&A or commercial law.

Other verticals (Supply Chain, Construction, Manufacturing) are present but fragmented.

Enterprise AI: This category shows a high degree of homogeneity. Solutions cluster around Sales, Marketing, Customer Support, and Knowledge Base Search. There is a lack of novel "ideas"; success here is now determined by product iteration speed, workflow integration, and GTM (Sales/BD) execution.

Consumer AI: We have yet to see a breakout "super app." Most projects remain focused on personal AI assistants aiming to improve individual work or life productivity.

Models, AI for Science, & Robotics: The number of companies in Models and Infrastructure is low, as the landscape is largely settled by established giants. Opportunities here are reserved for high-differentiation plays.

Series A/B - Established For Less Than 5yrs

This section focuses on the Series A/B stage, which represents the largest pool of companies in our dataset. We also include relevant Series C+ companies here for context. Series A remains the most challenging milestone in venture capital, serving as the crucible for validating Product-Market Fit (PMF) and scalability. Series B follows as the stage to accelerate and amplify that validated model. Therefore, the trends dominating this pool represent areas with verified commercial demand and genuine growth potential.

The Model Layer: Intelligence & Modalities

Pushing Reasoning & Intelligence: While big tech dominates general intelligence, startups are carving out niches by improving mathematical reasoning as a proxy for general intelligence.

The Math Path: Companies like Harmonic (co-founded by Robinhood’s CEO) and Axiom Math (founded by Carina, a "whiz kid" entrepreneur), as well as DeepSeek, are pursuing this path. This mirrors last year's trend of using Coding capabilities to boost reasoning.

Open Source: With Llama’s dominance challenged, startups like Reflection AI are attempting to build a "US version of DeepSeek."

Image & Video: Tools like NanoBanana have shifted image generation from "toy" to "tool." We anticipate a similar breakthrough for video models next year, which will trigger an explosion of video-native applications (we are already seeing "AI Ads" startups clustering in the latest YC batch).

World Models: Two distinct paths have emerged. One focuses on real-time video generation for entertainment and gaming (e.g., Decart AI). The other focuses on explicit 3D structures for robotics and autonomous driving.

Infra & Ops: The Revenue Hyper-Growth

Inference Platforms (Explosive Growth): Driven by open-source models, this sector has seen massive valuation and revenue jumps.

Together AI: ARR surpassed $300M

Fireworks: ARR hit $280M in their latest round (up from just $6.5M in April of the previous year)

Fal AI: Focused on multi-modal inference, they grew ARR 60x to $95M by their Series C in July. By December (Series D), ARR hit $200M, tripling their valuation from $1.5B to $4.5B in just four months

Training Data:

Mercor: Originally an AI recruiting platform, they leveraged their talent network to pivot into expert data labeling and model evaluation. They are one of the fastest-growing startups, projecting $750M revenue this year and $2B next year. (Peers like Surge, Turing, and Snorkel also closed large rounds).

Productized Data: David AI (Voice model data) stands out by shifting from a service model to a product model—proactively building standardized data products rather than waiting for custom client requests. They closed three rounds post-YC S24, reaching a $500M valuation.

Agent Infrastructure:

Search: Parallel, Exa, and Tavily are building the "Google for Agents."

Execution: Browserbase provides browser infrastructure for agents; Supabase provides the backend for "vibe coding" apps (like Lovable); n8n and LangChain provide the orchestration frameworks.

Enterprise Applications

Cybersecurity (32 Deals Tracked):

Agentic SOC: Moving from traditional tools to AI Agents handling "non-human" repetitive work. 7AI closed a $130M Series A (the largest in security history) at a $700M valuation. Cyera (Data Security) hit a $9B valuation.

GenAI Security: A new stack for new threats. LLM Vulnerabilities: Irregular ($450M Series A) detects model flaws for developers (clients include OpenAI/Anthropic). Social Engineering: Adaptive Security (protecting employees) and Doppel (protecting brands/anti-fraud) both closed consecutive rounds to fight Deepfakes and impersonation.

Sales & Marketing Innovations:

GEO (Generative Engine Optimization): Startups helping brands optimize visibility in AI chatbot answers (the new SEO).

AI User Research: Platforms like Listen Labs and Outset use AI to conduct automated user interviews (voice/video) and analyze sentiment, allowing rapid validation of business assumptions.

The "Reinvention" Thesis: VCs are buying into the "Reinventing Enterprise Software" thesis—replacing legacy systems like Netsuite with AI-native, intuitive tools. Compfire, Rillet, and DualEntry (AI-Native ERPs) each raised near $100M, targeting the new generation of tech companies.

The Implementation Gap: Distyl AI ($1.8B Series B) highlights a critical market reality: large enterprises (Telco, Mfg, Healthcare) need "Forward Deployed Engineers" to identify and implement AI use cases. This mirrors the trend seen in C3.AI’s financials, where high-margin professional services are in demand to bridge the gap between complex models and actual business value.

Vertical AI

Finance AI

The "Hippocratic for Finance" Trend: We are seeing a surge in platforms building comprehensive, industry-specific LLM applications, similar to Hippocratic's approach in healthcare. Companies like Rogo and the recently funded Model ML are leading this charge, securing significant capital to build "operating systems" for financial professionals.

Workflow Automation: The primary use cases center on corporate finance processes: Bookkeeping, Compliance, and Tax.

Sales Tax Niche: A standout sub-sector is Sales Tax automation, driven by the high complexity and frequent rule changes in the US tax code. Numeral (a YC W23 alumni) has reached a $350M valuation at Series B, joined by peers like Kintsugi AI and Zamp.

Healthcare AI

Development here focuses on three core flows: Patient Intake, Clinical Efficiency, and Revenue Cycle Management (RCM)

Startups are moving beyond diagnostics to tackle administrative friction points: Referral management, Medical Chart Review, Medical Coding, Prior Authorization, and Claim Submission. The goal is to use AI to automate repetitive tasks and ensure document accuracy to guarantee insurance payouts

Supply Chain & Logistics AI

Agentic Operations: YC-incubated companies like Happyrobot and FleetWorks are deploying Voice Agents to automate freight operations, order processing, and capacity planning. Happyrobot is notably expanding upstream/downstream into manufacturing and retail.

Macro Drivers: Tariff fluctuations are creating new opportunities for AI solutions focused on Supply Chain Compliance and Sourcing optimization.

Legal AI

With generalist giants like Harvey and Legora occupying the late-stage market, Series A/B opportunities have shifted to niche scenarios. We see activity clustering around IP/Patent protection and In-house Legal Automation (e.g., Eudia, Wordsmith AI).

DevAI

While "Coding Agents" and "Vibe coding" were themes throughout the year, the landscape is stratifying:

Coding Agents: With Cursor and Cognition dominating the late stage, Series A/B contenders are carving distinct paths. Factory targets enterprise-grade development teams, while OpenHands (formerly OpenDevin) pursues the open-source route.

Vibecoding: Beyond Lovable, Anything differentiates itself by building full-stack infrastructure rather than relying on third parties, ensuring higher reliability. Additionally, Vybe (YC W25) recently announced a seed round to bring vibecoding to internal enterprise apps.

Consumer AI

Emotional Companions: Portola, the developer of Tolan (an alien character AI), has found PMF by addressing "emotional overload" in younger users. Launched in February, it has over 5M downloads and reached $12M ARR by its July Series A. Similarly, Born’s Pengu (a virtual pet with social mechanics) has scaled to 15M global users by blending AI companionship with real-world social interaction.

Voice-First Interfaces: New interactions are being built on voice foundations, from Wispr Flow (Voice Input) to Sesame (AI smart glasses powered by voice models).

Embodied AI & AI for Science

Both sectors share a similar profile: high burn rates, extreme technical difficulty, and binary outcomes (massive potential or failure). The "Star Team" Dynamic: In Embodied AI specifically, the window for new entrants has largely closed. Major institutional investors have already placed their bets on "all-star" teams (e.g., Physical Intelligence, Skild AI, Genius AI), funding them heavily to wait for a breakthrough.

Series C - Established For Less Than 7yrs

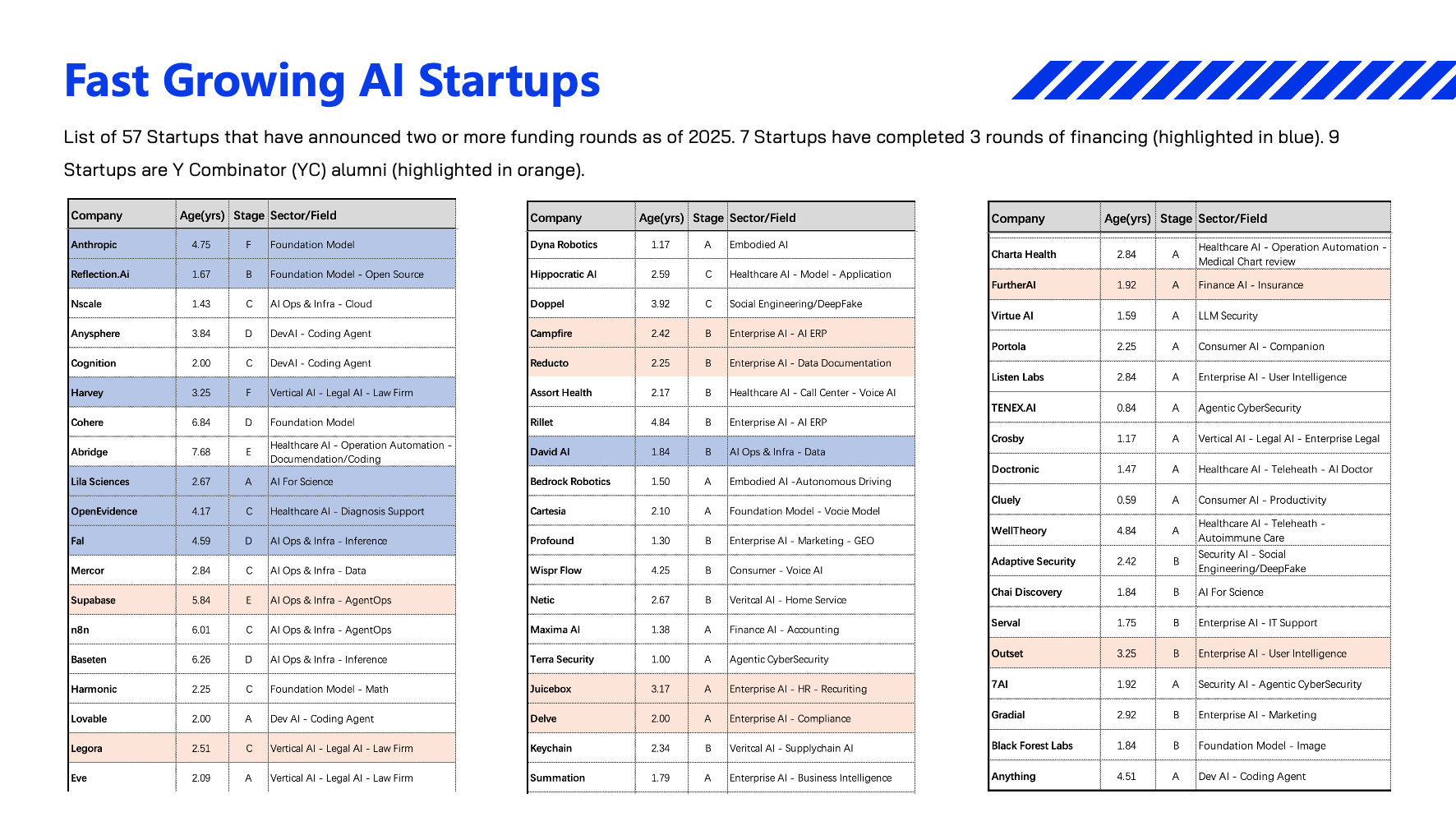

Fast Growing AI Startups

Shown above is a list of 57 projects that have announced at least two funding rounds as of December 2025. Key statistics include:

7 companies have completed 3 rounds (highlighted in blue).

9 companies are YC alumni (highlighted in orange).

Average Time to Milestone: Series A (2.06 years), Series B (2.49 years), and Series C (3.08 years).

We have previously covered the majority of these companies. Looking at the sectors they occupy, this list essentially serves to re-validate the trends and summaries outlined earlier in this report.